ECommerce in LegoLand

The shifting sands of modular vs. integrated stacks through time & space

Durian’s weekly thought to Ponder: “When shopping online, why has my customer UX remained so stagnant over the last decade?”

Morning all,

Apologies for the length, but after skipping last week and a full calendar next week, I felt entitled to a long one. Grab a coffee and enjoy.

This week, we explore:

The evolving war between modular vs. integrated ecommerce value-chains in different geographies - seen through the lens of “Dans. On the wall”

Amazon’s integration through logistics vs. Alibaba’s integration through aggregation

Why the U.S. has fallen behind: Fragmented payments & consolidated logistics vs. consolidated payments & fragmented logistics

Search vs Social vs Algorithmic front-end: Why the evolving modular eCommerce stack is hand-crafted for social platforms and backward integration

Southeast Asia: a Chinese-style integrator poised for war with U.S. social early in the eCommerce adoption curve

A recurring theme in my writing is drawing comparisons from the US and Chinese tech scenes to inform predictions in India and Southeast Asia. The crystal ball of history is a useful forecasting tool, but only when solving for localizations - differences in politics, technology, demographics, regulation, competitive environment - across geographies and time.

I’ll caveat up front; this week is ambitious in scope. Broad strokes are required to paint the evolving eCommerce value chain across the United States, China, and Southeast Asia in a book sleeve meant for the Iliad, let alone a single post. Incrementally, there are readers who are likely more familiar with the nuances of Chinese merchant tools or US payments or SEA last-mile which may be irked by the 20,000 foot view painted below. Be gentle. I’m aiming for the forest, not the trees. Tying it all together is why they pay me the big bucks (disclosure: 0 bucks).

***

To those who follow Stratechery, I will be riffing a bit off Ben Thompson’s post on The Anti-Amazon Alliance - integrators vs modular value chains in eCommerce - while exploring evolutionary paths across different geographies. The unique paths integrators (AMZN, BABA, SE) took on their journey can provide a lens into the vulnerabilities to backward integration of the modular stack by social players and the probability of their ascendance vs. the now dominant search-based integrators.

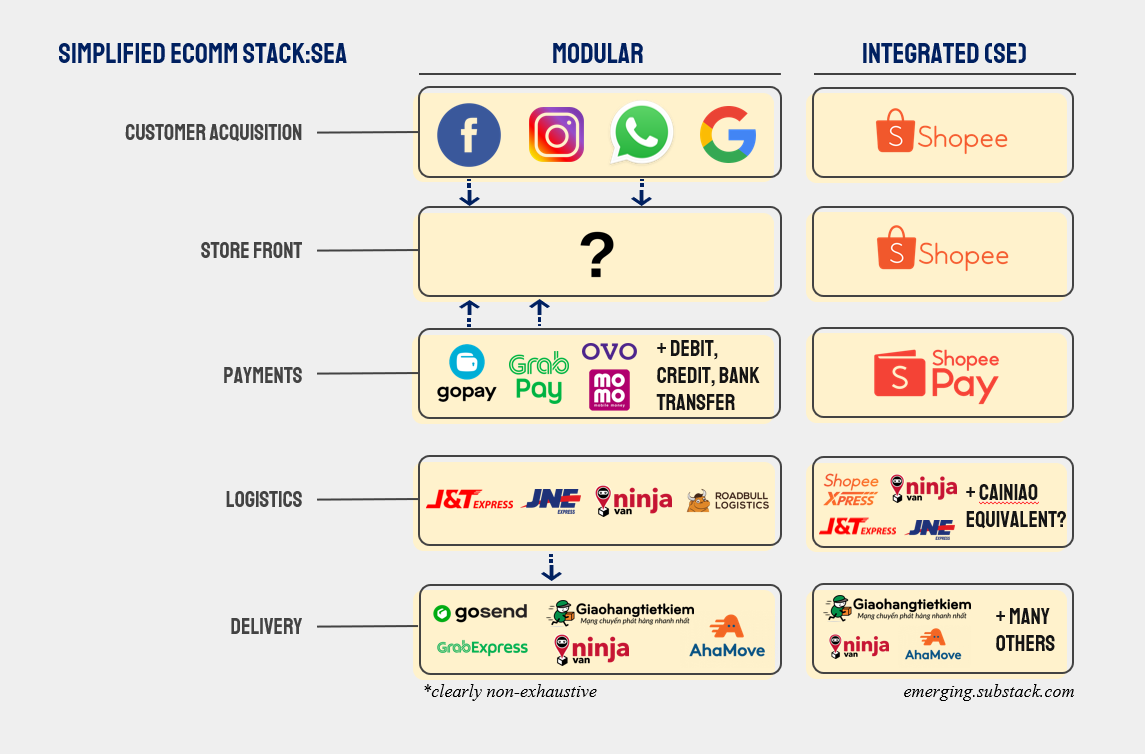

The eCommerce Stack: Modular vs Integrated

We will keep it high level and reduce the insanely complex eCommerce value-chain down to the same buckets as Ben: customer acquisition, storefronts, payments, logistics and delivery:

In the middle, you see a sample of the leading businesses which construct the building blocks of the “modular stack”. On the right-hand side, you can see Amazon’s competing integrated offering at each level.

Say I’m a sneakerhead. Vintage is in. Eco-friendly materials are top of mind. I think there’s a market in the US for quality, reasonable cost, vintage, eco-friendly Vans-style sneakers in California. Despite the looming lawsuit, I launch “Dans. On the wall”. I have two options: 1) Amazon. Amazon sources customers. Amazon houses my online store. Amazon takes care of the payments. Amazon takes care of fulfillment. Amazon takes care of delivery.

Three months in, business is great. My Dans “On the wall” are flying off the virtual shelves, and I’m about to order new inventory from my Brazilian suppliers when, all the sudden, I notice a down surge in orders in my Amazon analytics. I go online to investigate. Sadly, it appears Amazon is now selling very similar… maybe even identical… private label sneakers at a ~15% discount to my Dans. School of hard knocks lesson 1: I need to own the relationship with my customer.

Option 2.

Screw Amazon. I spin up an online store using Shopify, use Facebook and Google to target eco-conscious, aspirationally-hip product guys in the Mission (SF), seamlessly integrate with Stripe to accept payments online, and partner with 3PLs for easy delivery from a warehouse I have never seen. Magic. I’m up and running again within 72 hrs, but with more ownership over my customer relationships (fn.1).

This dynamic - an integrated vs modular value-chain for selling online - is not unique to the US. By examining the path of the integrator in each geography, we can began tease out clues as to how the coming war may evolve.

Amazon: Integration through logistics

In the US, Amazon’s rise went hand-and-hand with the early days of the internet. Founded 13 years before the onset of the mobile revolution. Before “blitzscaling” was a class at Stanford. Before the terms “Facebook” and “Google” were invented. Before the glitzy world of “network effects”, “aggregation theory”, and “mobile revolution”. Amazon’s DNA is in the real world.

Started as a 1st-party online retailer whose competitive differentiation was, and is, better experiences and lower prices through superior logistics. Upfront investment in logistics = superior customer experience = more brand loyalty = more customers which enabled Amazon to later add marketplace and payments into a fully-integrated offering. The capital markets have rewarded this flywheel with near infinite capital to continue to invest in even better logistics, better customer experiences, and deeper moats.

Amazon - at its core - is a logistics company. Given its strategy, dominance, and continued investments since the early days of the internet, the rest of the logistics industry in the U.S. was never able to catch up. Integration through dominant logistics was the path.

Chinese integration looks a bit different.

Alibaba: Integration through Aggregation

As opposed to Amazon’s logistics-first approach, Alibaba has always been more internet native. A classic digital aggregator first & foremost. Alibaba started from building liquidity at the top of the stack (storefronts & customer acquisition) and worked its way down.

Founded as a Alibaba.com - a B2B marketplace focused on connecting China’s SMEs with the outside world, Alibaba caught fire launching Taobao in 2003 - a C2C marketplace connecting China’s massive SMB and consumer segments online for the first time. The TaoBao platform allowed merchants to reach more customers online while simultaneously providing this expanding customer base a vastly superior product selection - all for free! (ads). Digital payments through AliPay was a natural extension, reducing friction and adding fuel to the accelerating flywheel. Integration from the top of the stack on down.

In its early years, logistics - the core ingredient to Amazon’s success - was largely left out of BABA’s vertical integration. Alibaba has brought the asset-light, TaoBao approach to logistics. The rise of eCommerce in China gave rise to a simultaneous explosion of 3PLs and delivery network partners to quench the thirst of the Alibaba flywheel and the insatiable Chinese consumer sending eCommerce penetration to unseen heights. As opposed to the heavy “in-house” logistics route taken by competitor JD, BABA leveraged its massive demand to foster cut-throat logistics competition. This Darwinian arena of gladiatorial combat for BABA’s volumes led to a sprawling, decentralized, and competitive logistics network which Alibaba does not own, but is now trying to tame with its Cainiao Smart Logistics Network.

Similar to TaoBao, Cainiao does not own assets, but connects the sprawling array of logistics partners from merchants, to first-mile, to warehouse operators, to long-haul, through last mile delivery. If you want access to Taobao’s massive volumes, partners must dance to the beat of Cainiao’s drum. Cainao is the digital backbone of Chinese eCommerce logistics which collects data, connects partners, suggests routes, and tracks packages through the chain - while relying on partners for the dirty work in the world of atoms. A pioneering approach to digital logistics.

While asset-light allows for rapid scaling and better returns on capital, outsourced logistics does not provide the same moat as in-house. The network is dependent on a dominant position in demand generation at the top of the funnel. However, what happens if say - Douyin pushes hard into eCommerce? Or PinDuoDuo leverages WeChat distribution to scale a massive audience? The logistics partners are mercenaries - loyal to the volumes and best pricing. Today that is BABA, but the sands shift over time.

As opposed to Amazon’s outright ownership, Alibaba’s flywheel at the top of the funnel is what allows for streamlined coordination of a sprawling array of parties downstream. However, Alibaba realizes this vulnerability and has been tightening its hold on core partners - increasing stakes in Cainiao (now 63%) and leading express delivery partners like Best Logistics (28%), STO (15%, recent option for 46% ownership by ~2022 just announced), YTO (23%, as of 9/1) and ZTO (10%).

In a way, Alibaba’s superior product evolution at the top of the funnel relative to Amazon’s - rapidly moving into live streaming, social, nuanced recommendation engines etc - is because it doesn’t have the same moat in logistics.

The evolution of non-captive logistics, along with seamless payments, are the two pillars which make China the most competitive eCommerce market on earth.

Payments, Logistics, Social and Backward Integration

In an April tweet, Bill Gurley highlighted exactly these two pillars as the key missing ingredients to the US eCommerce ecosystem:

As we have explored, there are a few reasons behind the divergence:

Bucket 1: Logistics

Amazon’s dominance and heavy capex investments since the early innings of US eCommerce led to less competition relative to Alibaba’s “asset-light” approach which fostered a more open logistics environment

China’s population density, lack of offline retail (~1/10th the US), and surging eCommerce penetration (#1 globally) created a virtual flywheel for logistics. More density = better cost structure = more profits = more competition = better customer service = more customers = more density

Our second pillar, frictionless payments, was also a key ingredient to the above flywheel.

Bucket 2: Payments

I have explored this quite thoroughly in Blitzscaling Credit as well as Chasing Ant, but the short story is AliPay and WeChat Pay leveraged massive user bases at the outset of the mobile revolution to blitzscale digital payments - wrestling power from the banking system - and centralizing payments (and increasingly digital financial services) into single platforms. Given the dominance of cash at the time, digital wallets were 10x better and gained rapid adoption. Ubiquitous, digital payments, largely external to the legacy banking system, concentrated in just two players, is what makes China’s seamless digital payments possible.

In comparison, the US bank-card centric payment system was birthed in the 1960s - before the modern internet. The legacy tech, fragmented players, entrenched interests, and established consumer behaviors mean closed loop digital ecosystems never had a chance to flourish. The pain of inputting credit card information at each site is the result of this fragmentation & legacy tech. By restricting your shopping to just a few sites - like say Amazon - you can avoid this hassle.

Search vs. Social vs. Algorithmic

Today, search-based commerce is clearly dominant globally and largely consolidates behind a single integrator. However, the time is ripe for a resurgence in discovery-based shopping. Online.

Connie Chan from a16z encompasses the phenomenon succinctly in this twitter thread. Highlights below:

Essentially, today’s champions have thrived in search-driven eCommerce: I know what I want, and I start banging away on the search bar on Amazon, TaoBao or Shopee. However, by reducing logistics exclusivity and payment friction, power can flow to any platform with eyeballs.

In Facebook, Jio, Gojek & the Coming War, I detailed the evolution of eCommerce from 1P (1.0) -> Marketplace (2.0) -> Social (3.0). Depending on how you view TikTok / Douyin, we may need to add (4.0): algorithmic. The coming clash between social / entertainment networks and search-based eCommerce aggregators has been well-documented. Nowhere is it more apparent than in China’s live-streaming war. ECommerce platforms are pushing hard into live-streaming, entertainment platforms are pushing hard into eCommerce. The competitive landscape is blurring fast.

The reason goes back to our modular stack. Shopify would claim their mission is to empower small merchants by providing the tools to go independent - avoiding the oppressive snare of the big, bad integrator. However, the way I see it, the emerging modular stack is purpose built for social platforms. Either small Shopify merchants will need to pay Facebook for customer acquisition (see footnote 1) or the pieces will be in place for Facebook to begin backward integration into Storefronts (Facebook Shops, WhatsApp for business, Facebook Checkout). The same applies to WeChat, Douyin, Kuaishou, Snap - you name it.

China’s eCommerce landscape is more dynamic largely because it has the two missing ingredients - seamless digital payment and more open logistics. WeChat, Douyin, Kuaishou and others are now sitting atop these pillars and peering over at the massive eCommerce pie a few integrations away. They have the customer acquisition. They have the payments. They can use the logistics. They only need to attract supply… which, it turns out, isn’t that hard when you have billions of eyeballs coming to your app. Bumping yourself from affiliate fee to eComm platform, simply by adding in-app checkout, just makes sense.

Unfortunately, the fragmented payments and concentrated logistics of the US ecosystem present the exact inverse of China’s concentrated payments and open logistics. Until that changes, it’s hard to see a discovery-commerce challenge to Amazon in the U.S.

Southeast Asia - Chinese eCommerce & Western Social

It seems odd in hindsight. Alibaba bought Lazada - the “JD.com” of Southeast Asia. Tencent then went and backed Shopee - “the Alibaba” of Southeast Asia. Now Shopee is pulling away from its Alibaba-backed rival using its own playbook. You can’t make this stuff up.

Shopee, the leading integrator, is executing the Alibaba playbook to a T. They skipped 1P and went straight to marketplace, pooled merchant and consumer liquidity online, added ShopeePay to accelerate the flywheel, and are going asset-light on logistics - linking with local partners to manage the world of atoms. I think we know the roadmap for this “search-based aggregator”.

The more interesting question is the maturation of the competing modular stack. Specifically, the “Shopify / Baozun” equivalent slot which is being encroached upon from above and below:

As Shraeyansh Thakur has pointed out in India:

The “Jio effect” has brought millions of Indians online in the last two years, and for many of these new mobile-first users WhatsApp is the internet, YouTube is television - and personal referrals from family and friends play an outsized role in how they discover new products in this digital world.

This has turned social platforms into powerful distribution channels for many businesses who are leapfrogging web and going digital with social-first models.

A similar dynamic is happening in Southeast Asia. The Facebook suite - Facebook, Messenger, Instagram, and Whatsapp - are often the first four apps downloaded on any device and effectively serve as a gateway to the internet. Despite poor tooling, these apps facilitate as much as ~50% of eCommerce through informal digital channels.

A goldmine.

While the Shopee search-based aggregation flywheel is kicking into gear, formal eCommerce penetration in India and Southeast Asia is just ~5 - 7% of retail. There is a massive untapped opportunity for social to jump into the fray before customer behaviors change. The thing is, social commerce is a more seamless fit with existing behaviors in the emerging world. From a post a few months back:

For many of these micro-businesses, this “push” approach - leveraging a hyper-local social graph - provides an easier transition to the online world relative to a traditional aggregator. Social is a more natural extension of their offline footprint and more closely mirrors the flows of today’s economy…

As opposed to roping all merchants into one, centralized aggregator, Facebook’s tools can serve as a spider-web of social ties - infiltrating the local-pockets of demand and trust to facilitate omni-channel transactions

Combatting traditional aggregators with the below “distributed network” (repaste) is why Facebook is investing so heavily in payments, FB shops, and WhatsApp for business in India and Southeast Asia:

It won’t be just Facebook, but any social / entertainment network which merchants will be keen to engage. Interestingly, this will bring them smack into competition with the current digital O2O champions - Grab, Gojek, and others - who hope to leverage payments as a foothold into incremental merchant services. Why should Facebook reap the benefits of O2O and hyper-local social commerce? Facebook is coming down the stack, while local champions are creeping up from below.

It will be fun to watch.

Without payment licenses and offline integrations, Facebook was always going to need local partners, but that doesn’t mean they will give up storefronts easily.

Given the digitizing payments and the open logistics in Southeast Asia, perhaps Shopee’s biggest threat is not Lazada, Tokopedia, or Tiki. Perhaps Shopee’s biggest threat is an awkward partnership between Facebook & Gojek / Grab pushing hard into hyper-local discovery.

Given search-based eCommerce is still only in its early innings, the best time to start is now.

***

Disclosure: I’m long Facebook

Footnotes:

(1) Unfortunately, there’s no real differentiation to my brand now that everyone has access to the same tools. New competitors Tans and Lans see my traction at Dans and tap the exact same strategy and supply chain. Given no differentiation, we compete for customers on Facebook, bidding up the auction price for eco-friendly sneakerheads in the western United States. Facebook and Google run away with the profits and sadly Dans and Tans go under while Lans is bought for a paltry sum by Boardriders in an unsuccessful bid to “revamp” their fading brand portfolio. Lesson 2: The modular platform may be slightly better than the vertical integrator, but either way, the small merchant is increasingly commoditized…

***

Emerging is a newsletter going deep at the intersection of tech & finance in Emerging Asia. Subscriptions are free & delivered to your inbox weekly. Prior musings can be found here.